The difference between a standard execution and a highly profitable one can come down to how effectively a lender can aggregate and hedge their production.

As interest rate fluctuations continue to challenge margins, understanding the nuances of the mortgage pool has become a critical competency for capital markets teams.

It’s all about the end price and how much you’re passing through. In this very competitive market, and as lenders try to compete for fewer loans, we’ve got to get more creative on what we can pass through to the consumer.

In this article, MCT’s Paul Yarbrough, Senior Director, Head of CSG & Analytics, and Jessica Visniskie, Director, Client Success Group, break down the mechanics of MBS pool optimization, the growing complexity of specified pay-ups, and how MCT’s next-generation Pool Optimizer is helping lenders capture the best execution.

What is an MBS Pool?

At its most basic level, a Mortgage-Backed Security (MBS) pool is a collection of individual home loans grouped together to serve as the collateral for a security.

Think of MBS pooling as a “bucket” of mortgages. Instead of selling one loan at a time, lenders group them so they can be sold to investors as a single financial product. Investors are drawn to the MBS pool because they offer a unique combination of safety and return.

When homeowners make their monthly mortgage payments, that money flows through the pool to the investors as monthly income.

Agency and Ginnie Mae securities are unique because they are either explicitly or implicitly guaranteed by the federal government and have historically offered higher yields than Treasury bonds with similar duration.

Agency MBS comprise one of the largest sectors of the U.S. fixed income market, with total outstanding balances measured in the trillions.¹ ² To put that scale in perspective, the Federal Reserve’s own agency MBS holdings of approximately $2.3 trillion as of mid-2024 represented nearly 30% of the entire agency MBS market alone.¹

The Science of Specified Pay-ups

In the secondary mortgage market, there is a baseline price known as “TBA” (To Be Announced). This is essentially the price for a “generic” or “average” security.

However, not all loans are created equal.

Some loans have specific “flavors” or attributes, such as a low original balance or a specific geographic location, that make them more attractive to investors because they are less likely to be paid off early.

When lenders group these high-quality loans together, they create a “specified pool” (or “spec pool”). Because these loans are more desirable, investors are willing to pay a “pay-up”, essentially a bonus, on top of the standard market price.

“A specified pay-up represents the additional price premium over TBA screen levels. When loans with desirable collateral attributes (such as low loan balance, for example sub-$85,000) are pooled together, the resulting specified pool commands a measurable premium relative to generic TBA pricing.”

– Paul Yarbrough, Head of Client Success Group and Data Analytics, MCT

Attributes for a Specified Mortgage Pool

Common attributes used to create a specified mortgage pool include:

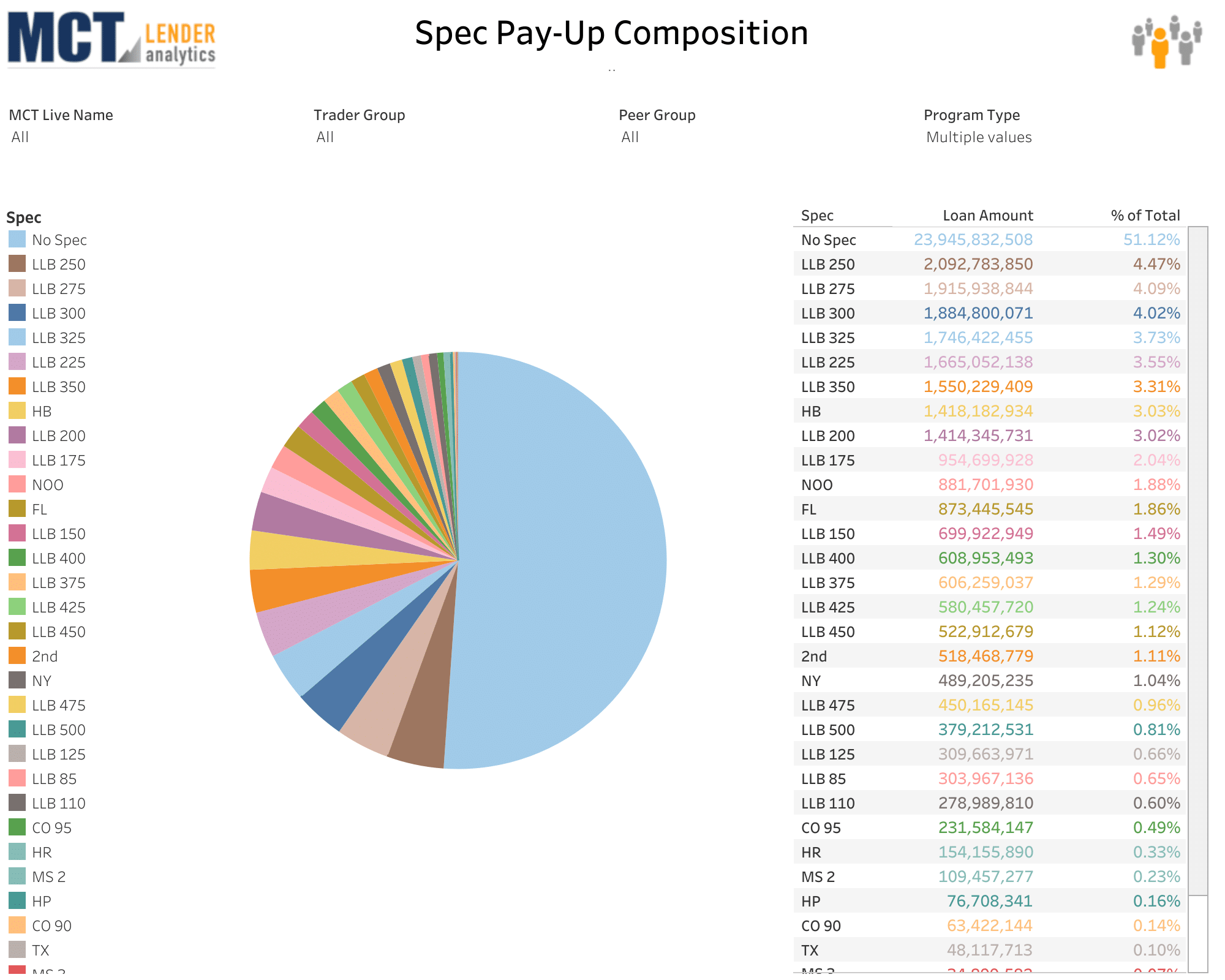

- Low Loan Balance (LLB): Loans under certain thresholds (e.g., $85k, $110k, $125k)

- Geography: Loans from specific states such as New York, Texas, or Florida

- Loan-to-Value (LTV): For example, Freddie Mac’s 94% LTV pay-up

- Credit Scores: Pools filtered by FICO scores

Per data pulled from MCT’s Lender Analytics platform as of March 31, 2026, approximately 48% of open hedged pipelines were represented by specified cohorts, with Loan Balance making up the lion’s share at 38%.

Why Volume Matters

Creating a specified mortgage pool isn’t as simple as just picking the best loans. There are strict rules, known as “constraints,” that lenders must follow. For example, to create a custom Ginnie Mae pool, you must have at least $1 million in total loan volume.

If a lender doesn’t have enough loans to meet that $1 million minimum for a spec attribute (like an $85k loan balance), they must use a “waterfall” strategy.

This means pool optimization is looking for the next best option, perhaps grouping those loans into a slightly larger balance category (like a $110k or $150k pool vs. $85k) to ensure the volume requirement is met while still capturing as much of the pay-up as possible.

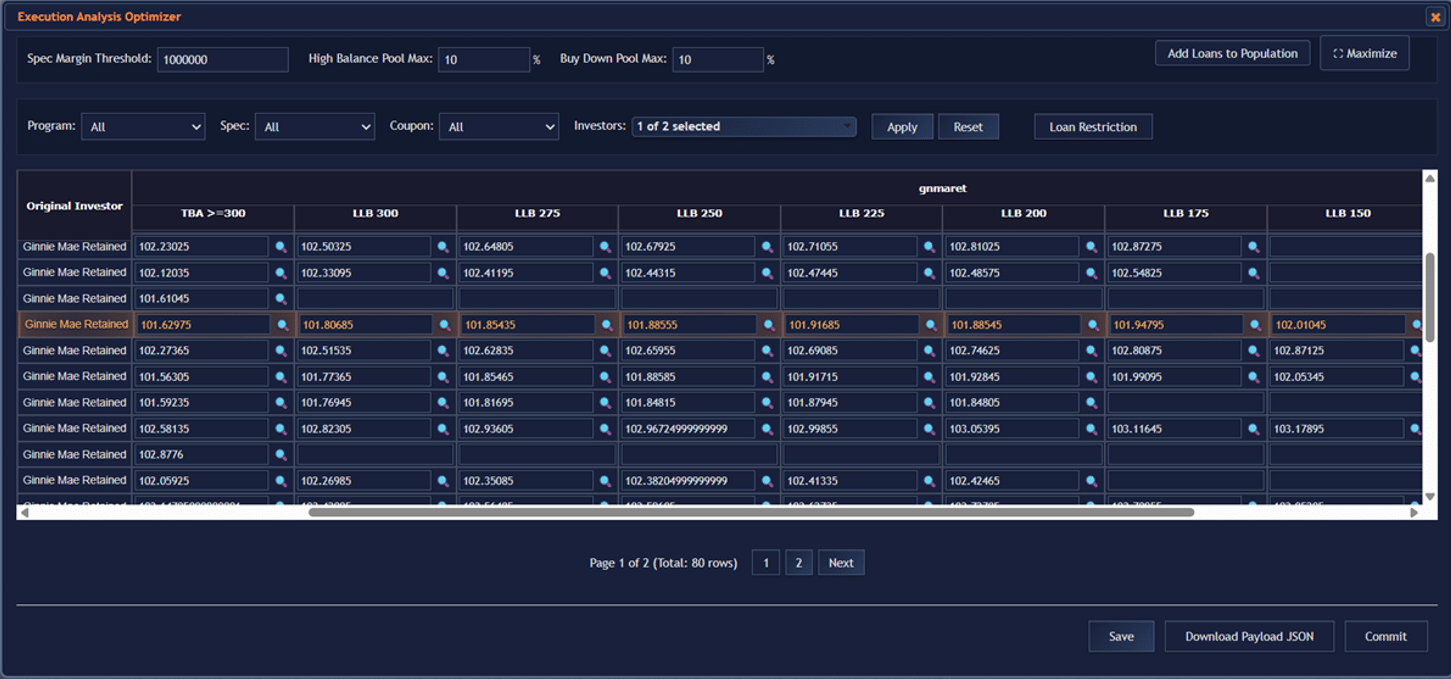

Overcoming Complexity with MCT’s Next-Gen Pool Optimizer

Trying to find the perfect combination of loans manually is nearly impossible. In a pool of just eighty loans with multiple delivery methods, each loan can only move down in category from the best possible price, so depending on where a loan sits it has roughly 4 to 20 possible assignments. 80 loans across 10 spec pool types and just 2 investors creates roughly 10^80 possible assignment combinations. That is equivalent to the estimated number of atoms in the observable universe!

To solve this, MCT recently debuted a next-generation Pool Optimizer powered by NVIDIA’s CUDA GPU framework, the same processing used for advanced AI tooling.

This allows the Pool Optimizer to run millions of iterations in seconds to find the most profitable path for every single loan.

This allows lenders to evaluate millions of iterations in real-time. As Paul Yarbrough notes, the speed of this technology is a game-changer for price discovery. “In an 80 loan pool, with 5, 10, or 30 executions, I may be creating 10,000 possibilities… that makes this more complex optimization possible in a way that’s never been done before.”

Hedging Spec Price Volatility

Because specified pool pay-ups can shift quickly, and sometimes independently of the broader rate market, lenders face a more nuanced risk than traditional hedging frameworks were designed to address.

At a high level, a loan’s price movement can be thought of in two parts:

- A Market Component: Driven by interest rates and captured effectively through TBA-based hedging.

- A Spec Component: Reflecting pay-ups, liquidity, and story-driven behavior that can cause loans to outperform or underperform the market.

Traditional regression models do a strong job explaining the rate-driven portion of that movement. But for lenders actively originating or trading specified collateral, the difference between how a loan should move and how it actually moves becomes increasingly important.

The difference between the two becomes spec risk.

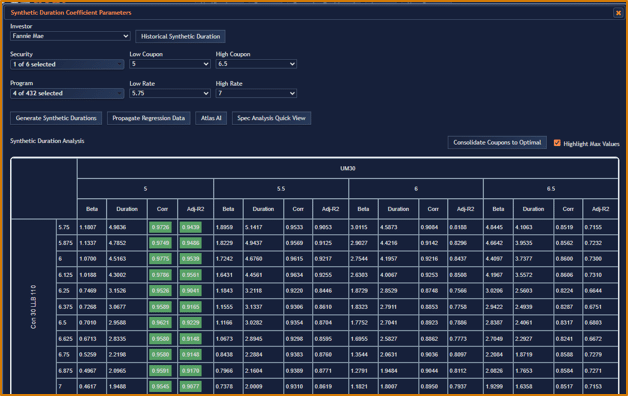

MCT’s Loan Duration Regression Analysis framework builds on this foundation by helping lenders isolate and quantify that behavior as actionable insight.

“MCT’s Loan Duration Regression Analysis tool gives you a strong baseline for how loans move with the market. What we’re adding is visibility into how specific stories — like loan size, occupancy, or geography — behave relative to the underlying market. When you can see that in near real-time, you can size your hedge more precisely and better protect your margins.”

– Jessica Visniskie, Director, Client Success Group, MCT

In practice, this can have a meaningful impact. In one observed period, the broader TBA market moved approximately 81 basis points, while a specified $110k loan balance pool moved closer to 94 basis points, roughly 15% more sensitivity than rates alone would suggest.

A standard hedge, calibrated only to the market component, would not fully account for that difference.

By incorporating spec behavior into the analysis, lenders can move beyond a one-dimensional view of duration and toward a more complete understanding of how their pipeline is likely to perform; ultimately enabling more precise hedge sizing, reduced P&L volatility, and improved margin preservation.

Conclusion

By using advanced technology to optimize mortgage pools, lenders can move beyond “average” pricing and capture significant premiums.

As a growing share of today’s loans meet the criteria for specified pools, the opportunity to extract additional value is becoming a core component of competitive execution. Lenders who can effectively identify and aggregate these spec-eligible loans are better positioned to capitalize on pay-ups that directly impact margins.

For lenders, using MCT’s Pool Optimizer to navigate these complex “buckets” of loans is the best way to ensure they’re maintaining competitive margins in a challenging environment.

Try MCT's Pool Optimizer

Whether you’re new to specified pool execution or looking to sharpen an existing workflow, MCT’s Client Success Group can walk you through the platform and help you evaluate where optimization can improve your pricing.

Read related articles below:

Sources:

- Board of Governors of the Federal Reserve System, “The Evolution of the Federal Reserve’s Agency MBS Holdings,” FEDS Notes, September 20, 2024. https://www.federalreserve.gov/econres/notes/feds-notes/the-evolution-of-the-federal-reserves-agency-mbs-holdings-20240920.html

- SIFMA Research, U.S. Fixed Income Securities Statistics — Outstanding. https://www.sifma.org/research/statistics/us-fixed-income-securities-statistics