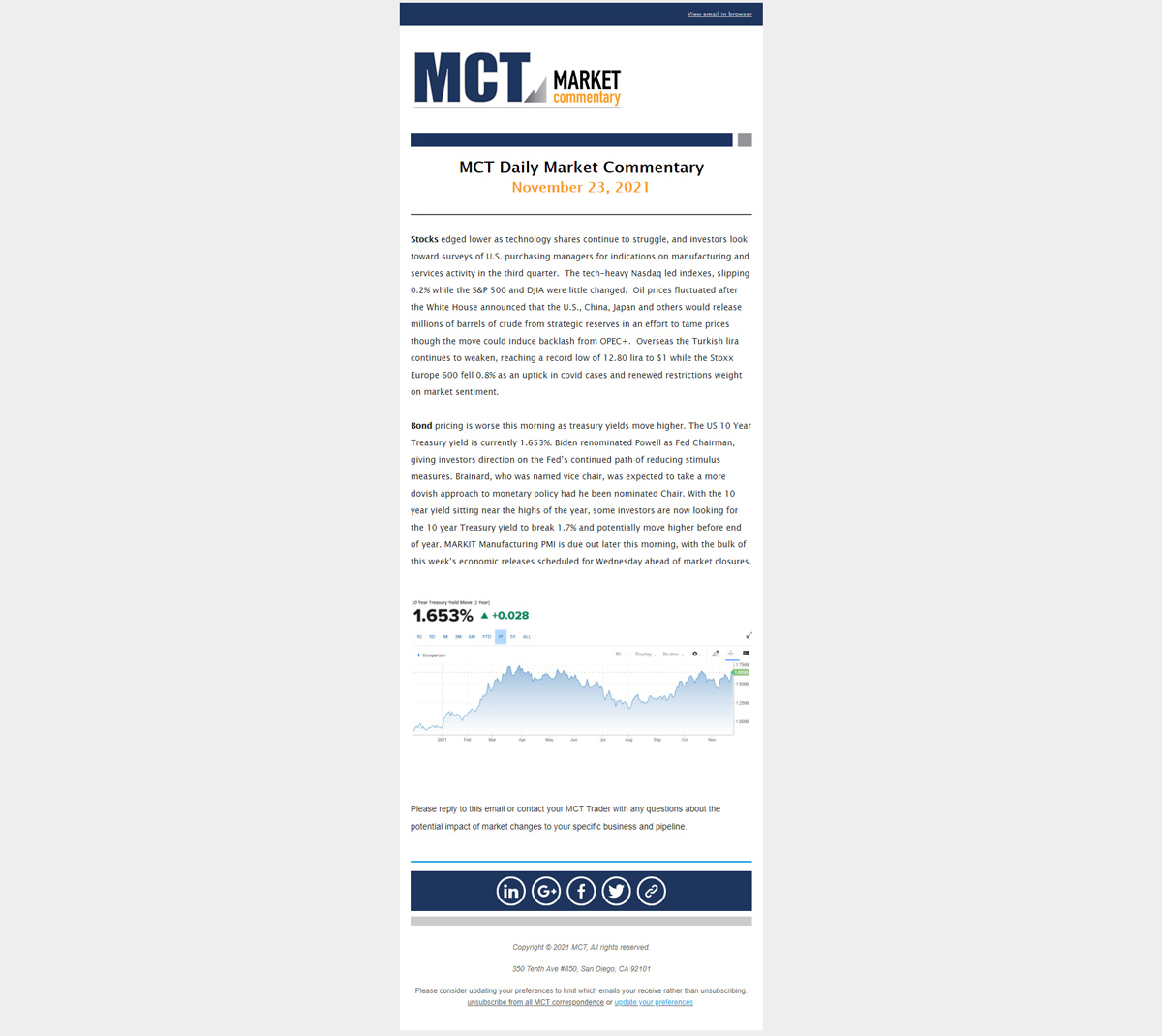

Treasury yields remain relatively unchanged despite minor fluctuations in both directions over the last two weeks. The Treasury yield curve steepened slightly with the 2-10 spread widening (by 4bps) to 0.54. The 10-year yield is currently 0.67%, and the 30-year is...

The US yield curve saw a sharp steepening after the Federal Reserve’s dovish statements from Jackson Hole. The plan, as described by Jerome Powell, Chairman of Federal Reserve, shifts the Fed’s focus away from a 2% inflationary target to concentrate on employment...

Long and intermediate Treasury yields edged lower last week as 30-year Treasuries experienced a 10-basis point drop while yield on the 10-year fell by 5bps. The accompanying 2-10 Year spread flattened by 5bps due to the 2-Year yield increasing to .16% on Friday....

Intermediate and long Treasury yields declined slightly last week, led by a 10 basis point drop in the 30-year bond yield. The 10-year yield declined by about 3 basis points, while the 2-10 year spread also flattened by 3 bps, as yields on maturities as long as five years remain pinned in place. In fact, the short end of the Treasury market has begun to reflect the possibility that the Fed will adopt so-called yield curve control this fall, a variation on quantitative easing where the Fed buys enough securities to cap the yield on a target maturity (generally assumed to be a short-term rate) at a certain level. What’s interesting is that the 5-year note has begun to trade as if its yield is (or will soon be) pegged, as highlighted by the accompanying chart. The graph indicates that the 40-day standard deviation of the 5-year yield is approaching its lowest level in years, only a few months after the pandemic-related market disruptions took the note’s volatility to levels last seen during the financial crisis of 2008-10.

Treasury yields declined modestly last week, led by intermediate and long maturities. The yield on the 10-year note dropped by a little more than 5 basis points, closing at 0.64%, while the 30-year bond yield closed 9 basis points lower to yield 1.37%. The yield curve also flattened a bit, with the 2-10 year spread narrowing by 3 basis points to 47.5 basis points. The 10-year TIPS yield (a proxy for the long-term inflation-adjusted or “real” yield) also declined to -0.69%, its lowest level since April 2013. A notable market development is the bottoming out of realized Treasury volatility, especially for the 5-year note. The chart below shows the 40-day standard deviations for the 5- and 10-year notes; while the 10-year has returned to mid-February levels, the 5-year note’s StDev recently approached its lowest print since mid-2018.

Treasury yields were little changed last week, with virtually the entire on-the-run curve closing within two basis points of the previous week’s marks. The 2-10 year spread ended the week a half basis point tighter at 50.6 basis points, while the 5-30 year spread widened similarly. The only notable changes were in the TIPS markets; while the 10-year breakeven rate (a measure of market inflation expectations) widened by just under 9 basis points to +1.29%, the yield on the inflation-adjusted 10-year note declined to -0.615%. Using the Treasuries constant-maturity index for the 10-year TIPS, this was its lowest reported yield since mid-2013 and reflects expectations for very low “real” interest rates in the future.

Severe gyrations in the stock markets left intermediate and long Treasury yields sharply lower on the week. The yield of the 10-year note declined by 19 basis points to 0.705%, leaving the yield curve noticeably flatter; short-maturity yields remained pinned in place, reflecting continued accommodative monetary policy. The Fed was, in fact, a major driver of the markets last week, as Thursday’s sharp equity selloff was precipitated by Fed Chairman Powell’s downbeat statement on the short-term economic outlook, as well as concerns that new waves of Covid-19 infections are brewing.

Treasury yields spiked higher last week, capped off with an extraordinary Friday session highlighted by an enormous miss by economists’ forecasts for the May employment report. Instead of losing the 7 million jobs predicted by a survey of economists, the job market actually added 2.5 million jobs. While the drop in the unemployment rate may have been overstated by misclassification of workers who were “employed but absent” from work, the report nonetheless highlights the enormous difficulties in predicting the short- and long-term path of the job market and the economy.

Treasury prices barely budged last week, with the exception of the very long end of the yield curve, which sold off modestly. The 10-year note ended the week yielding 0.65%, while the new 2-year continued to hover around the 0.15% area, ending the holiday-shortened week yielding 0.163%. The quietude in the Treasury market left the 10-year daily standard deviation at 4.2 basis points, just slightly higher than its level in mid-February when the S&P 500 posted its all-time high level. (For context, it did reach 12.3 basis points per day in early April, slightly higher than its peak in last 2008 and early 2009.)

Treasury prices held steady last week, even as equities sank in response to growing pessimism over the economic fallout from the Covid-19 pandemic. The 10-year Treasury yield declined by about 4 basis points week/week to yield 0.644%, while the 2-year yield plumbed its all-time lows to yield 0.147%. The 10-year TIPS break-even rate (i.e., a proxy for projected future inflation) dropped modestly to around 109 basis points (which roughly translates to just over a 1% long-term inflation rate); while very low historically, this measure is still well above its 95 basis point level reached in mid-April, not to mention the 55 bp level reached on March 19th at the height of the crisis.

The Treasury yield curve continued to slowly steepen last week, reflecting anxieties over the flagging economy and speculation that the Fed may begin to contemplate negative interest rates. The 10-year note finished the week to yield 0.685%, an increase of about 7 basis points over the previous Friday’s close, while the 2-year note closed at 0.16% after reaching an all-time low of 0.14% on Thursday. On that day the Fed Funds futures market reflected a -0.017% rate at the December 16th OMC meeting, as traders began to speculate what else the Fed might do to support economic activity with a jobless rate approaching 20%.

The Treasury market took a breather last week, leaving yields little changed. At 0.614%, the 10-year note’s yield closed a little over a basis points higher than the previous Friday’s level, while the 2-10 spread steepened by about 5 basis points, as the curve “twisted” mildly around the intermediate maturities. With Treasuries settling into trading ranges, their realized volatilities have started to decline.

The Treasury yield curve underwent a “twist” last week, as shorter maturity yields rose modestly while yields on longer Treasuries declined. The 10-year yield ended the week at 0.60%, lower by about 4 basis points, while yields on 2- through 5-year notes rose between 1.5 and 2 bps. The 10-year appears to be settling into a trading range of around 0.50-0.80%, while its 60-day standard deviation is also stabilizing at a little over 12 bps per day, and should start declining as the very volatile March sessions start to roll off.

Intermediate and long Treasury yields declined last week, as the Treasury market looks to be settling into a trading range after a period of extreme volatility. The 10-year yield dropped by about 8 basis points, leaving the 2-10 year spread narrower by about 6 basis points. The decline in the 10-year yield reflected a sharp decrease in the 10-year TIPS break-even (i.e. the projected future inflation rate), which moved in sympathy with weakness in oil prices.

Intermediate and long Treasury yields declined last week, although the extreme volatility in Treasury yields experienced over the last month dissipated a bit. The 10-year Treasury yield ended the week at just under 0.60%, while short yields either closed roughly unchanged (the 2-year note) or rose. (T-bill yields ended the prior week slightly negative, so the increase in the 3-month bill yield to 9 basis points was somewhat welcome.) The back-end rally reflected declining long-term real rates, as the yield on the 10-year TIPS dropped by 15 basis points while the Break-even rate (reflecting expected future inflation) rose by 7 basis points, suggesting that traders are not yet incorporating deflation fears into their thinking.

Treasury yields ended the week lower, although prices spent most of the week in negative territory before a big rally on Friday took the 10-year yield to its lowest level since 3/9. With Treasury bills carrying negative yields for much of the week and the 2-year note pegged in place at around 0.25%, the decline in yields was focused in intermediate and long maturities, leaving the 2-10 year spread flatter by about 10 basis points at +43 bps. (However, if anyone in the future cites last year’s mild yield curve inversion as a factor in the recession we’re likely to see later this year, please instruct them on the concept of “social distancing.”)

Treasury yields were lower week-over-week, but the apparently modest decline in yields does not begin to describe the volatility that the bond markets underwent last week. The chart below, which shows hourly pricing for the 10-year note from 3/13 through 3/20, indicates that the note’s price traded as high as 108-14 (on Sunday night 3/15 in Asia) and as low as 102-03+ on Thursday morning, traversing roughly a 6 ¼ point range over the course of the week. Not surprisingly, realized volatility continued to surge, with the 40-day daily realized vol on the 10-year closing last week at 12 basis points, triple what it was in mid-February.

Treasury yields ended another volatile week mixed, with yields on intermediate and long maturities rising while shorter maturity yields declined. After bottoming out at 0.54% on Tuesday, the 10-year note eventually ended the week yielding 0.96%, although the latter part of the week saw intense intra-day volatility. The rally in the short end of the curve, which pushed the 3mo/10yr spread wider by 40 basis points, likely reflected expectations of a sharp cut in the Fed Funds target rate by the Fed at the 3/18 meeting; the Fed ultimately jumped the gun with a rare (if not unprecedented) Sunday announcement of a return to a 0-25 basis point target. The Fed also announced other measures, including a tepid return of a Treasury purchase program on Thursday and a larger program with the Sunday announcement.

Yields around the world headed lower last week, as the powerful fixed income rally picked up steam. The 10-year note ended the week at a new record low yield of 0.76%, dropping by about 38 basis points week/week. The bond markets were boosted by a 50 basis point rate inter-meeting cut in the Fed Funds target, which sharply boosted pricing in the money markets, highlighted by a 78 basis point drop in the 3-month T-bill rate. By Friday’s close, the Fed Funds futures market was projecting more than two rate cuts at the 3/18 meeting, while Monday’s oil-driven rally has pushed the futures market to project the possibility of the 0% target rate seen from last 2008 through 2015.

The financial markets ended an incredible week with Treasury yields reaching new lows. The 10-year note at a yield of 1.15%, over 20 basis points lower than the previous low hit in the weeks after the 2016 Brexit vote. The 3-month/10-year spread further inverted by about 8 basis points to close around -11 basis points, while the 2-year/10-year spread expanded by 12 basis points to +23, its widest level since early January of this year.

Treasuries steadily rallied last week, with the 10-year note ending the week yielding 1.472%. The drop in yields, triggered by fears that the coronavirus was spreading outside of Asia, was focused in intermediate and long maturities, and left the yield on the 30-year bond at an all-time low 1.915%. The 2/10 year spread ended the week about 4 basis points flatter, while the 3mo/10 year spread inverted to close at -5 basis points. The yield on the 10-year TIPS (reflecting the expected long-term real rate) declined by 6.5 basis points, while the TIPS breakeven level (a proxy for projected inflation) also dropped by about 5 bps.

Treasury yields rebounded last week, although the market paradoxically rallied on Friday despite a relatively strong employment report.

Treasury yields plunged last week amid fears that the fast-spreading coronavirus would disrupt global trade and economic activity. With U.S. equities off by about 2.5%, the 10-year yield dropped by almost 18 basis points to end the week at 1.508%, breaching its early October lows and getting within 5 basis points of the late-summer trough. While yields for coupon-paying securities declined pretty much in unison, Treasury bill rates actually rose slightly, leaving the 3mo/10-year spread slightly inverted even though the 2/10-year spread closed roughly unchanged. Despite the Fed’s fairly neutral statement after their Open Markets Committee meeting on the 29th, the Fed Funds futures market is currently projecting a 25 basis point rate cut by as early as the June or July meetings, and two easings by the end of 2020.

Treasury yields dropped last week, as concerns about the spread of the coronavirus and its economic impact grew. The yield on the 10-year note declined by about 14 basis points from the prior Friday to yield 1.685%, with the rally concentrated in intermediate and long maturities. This left the yield curve markedly flatter, with the 3mo/10yr and 2-10yr spreads narrower by 11 and 7 basis points, respectively. The rally also took other sovereign yields lower; the German and French 10-year notes both experienced 12 basis points declines, the latter reaching negative territory for the first time since early December, as highlighted by the accompanying chart.

Page 4 of 6« First«...23456»