FNCL 3.0s opened the day at 101-03, hit a high of 101-12+ just prior to 12 noon, and then we drifted lower in the afternoon to close at 101-04. We saw some intraday reprices for the better in the late morning and then some in the other direction later in the afternoon. We are now about 6 ticks lower vs. the Friday close of 101-04 but do not expect much from TBA hedge flows today. March issuance is about ~2.0bln behind the pace of February when you compare the first four business day of March to those of February. The big drop occurred in February and I would now expect the attrition to be a few billion/month.

We’ve seen lighter supply thanks to the Russia/Ukraine headlines. The market has ultimately gained ground with FNCL 3.0s starting at 100-06+ and closing at 100-15. We did see some negative reprices, then the Russia/Ukraine headlines moved the bond market higher into lower yields and that brought better reprices. We currently have FNCL 3.0s at a lower closing level so don’t expect much.

MBS gave back gains from earlier in the week, better sellers and heavy supply pushed the basis down 3-5 ticks with weak demand throughout the session. Afternoon flows skewed towards fast money selling. FNCL 2.5 closed 4 ticks wider @ 99-21+, FNCL 3 also 4 wider @ 102-00+. G2/FN down on the day but fared better than conventional counterparts, 3.5s the only green swap on the stack up 2 ticks on better buying. 15yrs higher vs 30s by 2 ticks, bank flows have been light but steady.

Are We in for a Housing Market Correction? The start of 2022 has seen market corrections in risk assets, which has led to murmurs of a potential correction in home prices as the Federal Reserve’s tapering of asset purchases leads to higher mortgage rates. Housing prices have risen dramatically (nearly 20% nationwide, per Case Shiller and FHFA) over the past year, and even if many people feel that meteoric rise makes conditions ripe for a bubble, a closer look reveals that is not necessarily the case.

What to Watch in 2022. As traders return to action and open 2022, it is to a market dominated by increasing (milder?) COVID infections under the shade of inflation and tightening by the Fed. The last two years have shown that changes in COVID infections shift the economy, though each successive wave of infections has led to milder economic slowdowns.

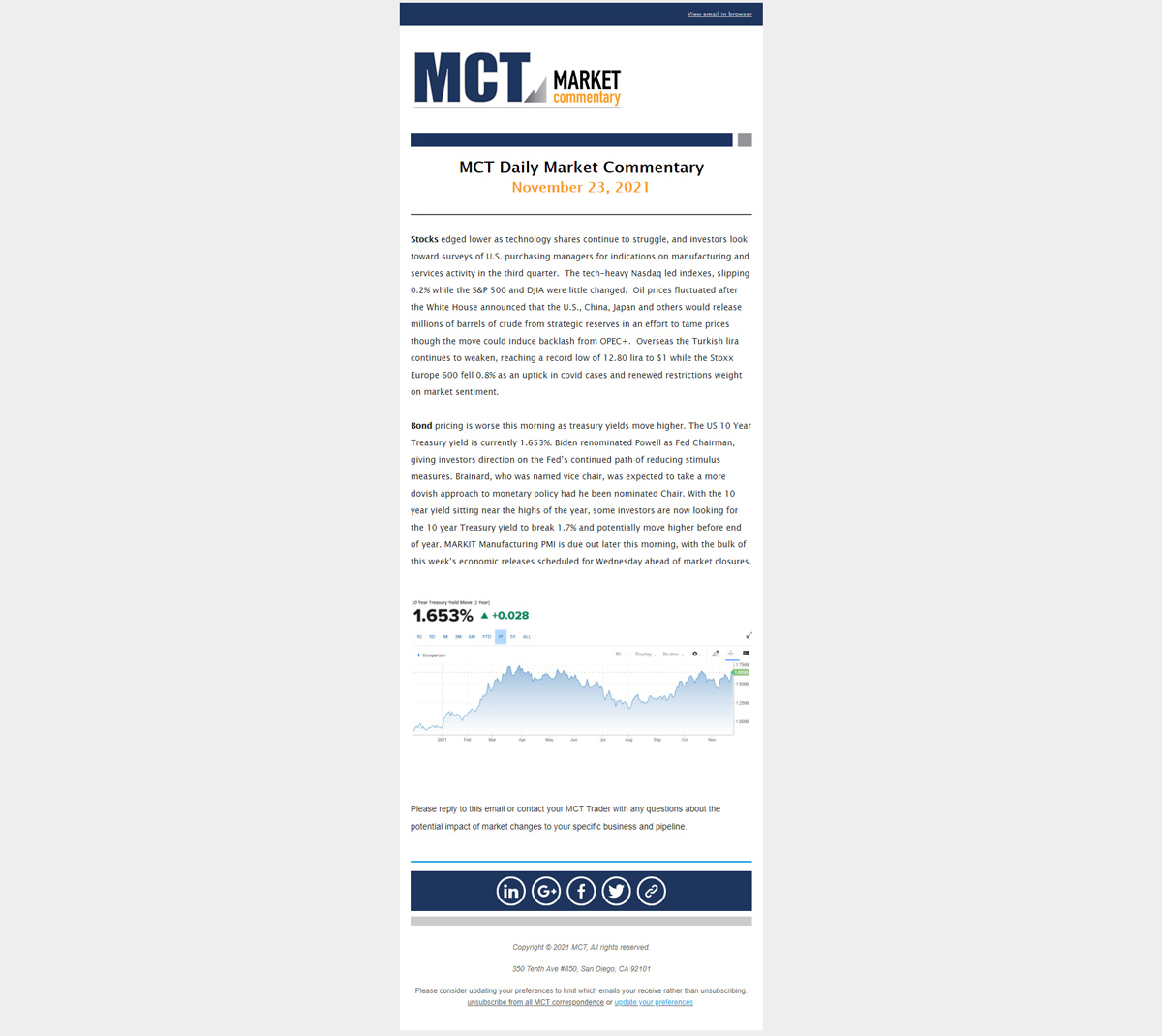

Long-term 30-year yields have fallen to 1.909 %, the 10-year is currently yielding 1.266%, and the Fannie Mae 30-year current-coupon spread to the 5/10-year blend widened to +73.

Long-term 30-year yields have fallen to 2.151%, the 10-year is currently yielding 1.46%, and the Fannie Mae 30-year current-coupon spread to the 5/10-year blend tightened to +70.

Long-term 30-year yields have fallen to 2.321%, the 10-year is currently yielding 1.621%, and the Fannie Mae 30-year current-coupon spread to the 5/10-year blend tightened to +64.

Long-term 30-year yields have fallen to 2.343%, the 10-year is currently yielding 1.628%, and the Fannie Mae 30-year current-coupon spread to the 5/10-year blend widened to +64.

Long-term 30-year yields have fallen to 2.29%, the 10-year is currently yielding 1.593%, and the Fannie Mae 30-year current-coupon spread to the 5/10-year blend widened to +63.

Long-term 30-year yields have fallen to 2.27%, the 10-year is currently yielding 1.583%, and the Fannie Mae 30-year current-coupon spread to the 5/10-year blend tightened to +66. Also of note, the US MBS index option-adjusted spread hit its tightest level in over a decade on Wednesday, closing at 7bps.

Long-term 30-year yields have fallen to 2.333%, the 10-year is currently yielding 1.662%, and the Fannie Mae 30-year current-coupon spread to the 5/10-year blend tightened 2 basis points to +68. The spread has tightened to its lowest in almost two months.

Long-term 30-year yields have risen to 2.405%, the 10-year is currently yielding 1.695%, and the Fannie Mae 30-year current-coupon spread to the 5/10-year blend widened to +80. Treasury yields continue to rise to their highest levels in over 12 months.

Long-term 30-year yields have risen to 2.382%, the 10-year is currently yielding 1.628%, and the Fannie Mae 30-year current-coupon spread to the 5/10-year blend widened to +73. Treasury yields continue to soar to their highest levels in over a year.

Long-term 30-year yields have risen to 2.304%, the 10-year is currently yielding 1.57%, and the Fannie Mae 30-year current-coupon spread to the 5/10-year blend tightened to +70. On Friday, yields on Treasuries closed at their highest in a year.

Long-term 30-year yields have risen to 2.169%, the 10-year is currently yielding 1.375%, and the Fannie Mae 30-year current-coupon spread to the 5/10-year blend widened to +77. Yields on Treasuries closed at their highest in almost a year.

Long-term 30-year yields have risen to 1.983%, the 10-year is currently yielding 1.182%, and the Fannie Mae 30-year current-coupon spread to the 5/10-year blend tightened to +65. The spread from the current coupon to Treasuries is the lowest in more than 19 months while yields on Treasuries closed at their highest in more than 10 months.

Last week’s Treasury selloff marked the quickest reversal in government debt yields since the collapse in March. The prospect of a unified Democratic representation in Federal offices fueled stimulus bets and contributed to a further steepening yield curve (See 5-30 Year Spread). Long-term 30-year yields have risen to 1.875%. The 10-year is currently yielding to 1.117%. The Fannie Mae 30-year current-coupon spread to the 5/10-year blend tightened to +67, the lowest in 18 months.

Intermediate Treasury yields fell 2bps to 0.83% to finish out the week. The 30-year Treasury is currently yielding 1.56%, relatively unchanged from the start of the week. The Fannie Mae 30-year current coupon spread to the 5/10 year blended widened 1bp to +76.

The 10-year Treasury yield rose to 0 .98% to begin last week, following the announcement of Biden’s victory. However, uncertainty continues to plague markets due to the absence of a standard concession and continued accusations of fraudulent voting. The uncertainty caused the 10-year to retreat to 0.89% by Friday. The spread between the 10-year Treasury to the 5/10-year blend has tightened 3bps to +72.

The 10-year Treasury yield rose to 0.85%, 5bps higher than start of last week. The 30-year Treasury is currently yielding 1.63%. The Fannie Mae 30-year current-coupon spread to the 5/10-year blend tightened 1bp to +80. Volatility has risen to its highest levels in about six months.

Intermediate and long-term Treasury yields crept up 10-12bps last week. The 30-year Treasury is currently yielding 1.61% and the 10-year is 0.84%. The sell-off in Treasuries was induced by increasing expectations for a stimulus package either passed before the election (unlikely), or by a democratic win in the election based on recent polls.

The Fannie Mae 30-year current-coupon spread to the 5/10-year blend tightened 2 basis points to +79 as the U.S. Treasury 10-year yield rose 3 basis points to 0.86%. The spread between FNMA 30-year 2 and the 10-year Treasury is the lowest its been in 15 months.

The 10-year Treasury closed 2bps higher on Friday and is currently yielding 0.69%. The 30-year Treasury also increased 3bps to 1.48%. 10-year TIPS yield tightened 1bp to -0.94%.

MBA’s weekly mortgage applications index fell 4.8% in the week ended Sept. 25 after rising 6.8% in the prior week. Purchases were down 1.9% and refinances fell 6.5% after rising 3.4% and 8.8% respectively, in the previous week. The average 30-year fixed rate is 3.05% – the lowest in survey history, according to the MBA. Compared to last year, 30-year fixed rates are down 77bps. Freddie Mac’s 30-Yr FRM is currently 2.88%, down 2bps since last week. Also notable, pending home sales jumped 8.8% in August, following a 5.9% increase in July.

Treasury yields saw subtle gains through last week. The 30-year yield increase from 1.42% to 1.45%, and the 10-year edged up to 0.70%. The 10-year TIPS yield remains at -0.97%.

Page 3 of 6«12345...»Last »